Understanding how changing interest rates and national monetary policy influence your personal finances can help you make decisions consistent with your financial goals.

On its face, an interest rate is simple: It’s the cost of borrowing an asset. Risk, timing, opportunity cost and the borrower’s creditworthiness factor into an interest rate. There are also components in the final rate that are market-driven interest rates influenced by national monetary policy.

THE POLICIES OF MONEY SUPPLY

Monetary policy is primarily concerned with the availability of money in an economy. In the U.S., it is guided by the Federal

Reserve System (Fed), which is mandated to promote maximum employment, stable pricing to limit inflation and moderate long- term interest rates. To achieve these aims, the Fed adjusts the federal funds rate.

The federal funds rate is the amount of interest financial institutions charge one another for overnight loans to meet the requirement for reserve cash holdings, and its rate impacts other interest rates on the open market.

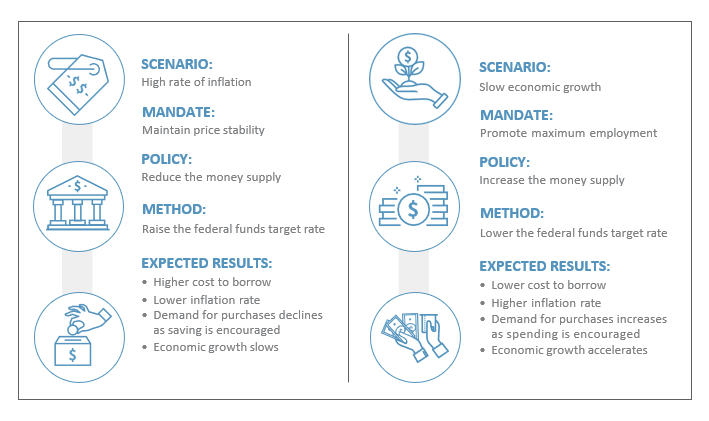

MANAGING ITS MANDATES

The Fed’s rate-setting authority influences nearly every part of our credit-heavy economy. As a result, the Fed manages a variety of scenarios that the economy may experience, including these examples.

MARKET-DRIVEN INTEREST RATES

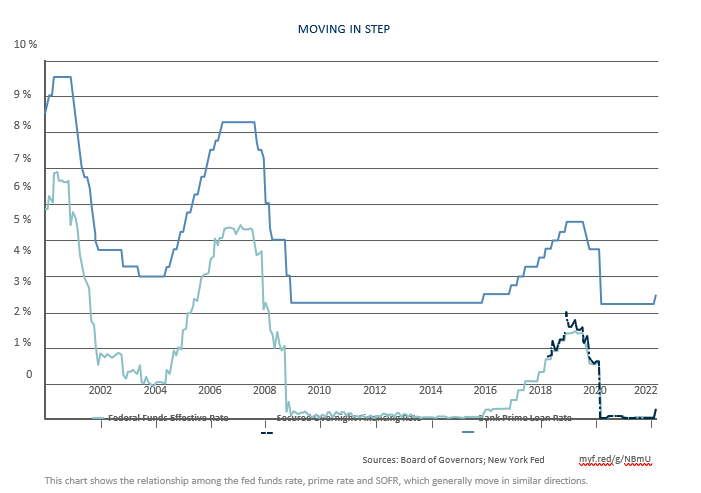

Though many lenders set their own interest rate benchmarks instead of leveraging the effective federal funds (EFF) rate, these rates are highly correlated with Fed monetary policy.

Here’s how two major benchmark rates have been impacted by EFF.

THE PRIME RATE

The prime rate is the benchmark interest rate that commercial lenders charge their most creditworthy corporate customers. This rate is the starting point for most types of lending, including:

- Mortgages

- Home equity loans

- Credit cards

- Small business loans

Each lender sets its own prime rate, but the average prime rate across all lenders tends to be 3 percentage points higher than the effective federal funds rate. Changes in the effective federal funds rate are typically reflected in the average prime rate almost immediately.

SECURED OVERNIGHT FINANCING RATE

The secured overnight financing rate (SOFR) is the benchmark banks use to set interest rates on U.S. dollar-based derivatives and loans. SOFR, created by the Fed in 2018, is based on actual transactions on the U.S. Treasury bond repurchase market. This rate is the starting point for several credit products, including:

- Securities-based lending

- Structured lending

- Margin lending

SOFR is highly correlated to the effective federal funds rate. Changes in the effective federal funds rate are typically reflected in SOFR almost immediately.

Products, terms and conditions subject to change. Subject to standard credit criteria.

Raymond James Bank is registered with the NMLS Registry and is authorized to conduct mortgage transactions under NMLS ID 405712.

Property insurance required. Flood insurance required if property is located in a designated flood zone of “A” or “V.”

Raymond James & Associates, Inc., Raymond James Financial Services, Inc., and your Raymond James financial advisor do not solicit or offer residential mortgage products and are unable to accept any residential mortgage loan applications or to offer or negotiate terms of any such loan. You will be put in contact with a Raymond James Bank associate for your residential mortgage needs. Raymond James Bank is not in any way responsible for the debts issued by or the obligations of an affiliate of Raymond James.

A line of credit backed by securities, such as a securities-based line of credit or a structured line of credit, or Margin account may not be suitable for all clients and investors. Borrowing on securities-backed lending products or Margin accounts and using securities as collateral may involve a high degree of risk, including unintended tax consequences and the possible need to sell your holdings, which may lead to a significant impact on long-term investment goals. An investor can lose more funds than he or she deposited in the account. Market conditions can magnify any potential for loss. If the market turns against the client, he or she may be required to quickly deposit additional securities and/or cash in the account(s) or pay down the loan to avoid liquidation. Clients and investors may not be entitled to choose which securities or other assets in his or her account are liquidated or sold to meet a call. The firm can increase its maintenance requirements at any time and is not required to provide advance written notice. Clients and investors may not be entitled to an extension of time on calls. The securities in the pledged account(s) may be sold to meet the collateral calls and the securities in a margin account can be sold to meet margin calls; the firm can sell the client’s securities without contacting them. Increased interest rates could also affect SOFR rates (or any successor rate thereto) that apply to your line of credit, causing the cost of the credit line to increase significantly. The interest rates charged on a line of credit are determined by (i) the market value of pledged assets and the net value of the client’s non-pledged Capital Access account or (ii) the line of credit amount. The interest rates charged on margin accounts are determined by the amount borrowed. Please visit sec.gov/investor/pubs/margin.htm for additional information.

The proceeds from a securities-based line of credit or a structured line of credit cannot be (a) used to purchase or carry securities; (b) deposited into a Raymond James investment or trust account; (c) used to purchase any product issued or brokered through an affiliate of Raymond James, including insurance; or

(d) otherwise used for the benefit of, or transferred to, an affiliate of Raymond James. Raymond James Bank does not accept RJF stock or any securities issued by affiliates of Raymond James Financial as pledged securities toward a line of credit. Lines of credit are provided by Raymond James Bank. Securities-based line of credit and structured line of credit provided by Raymond James Bank. Raymond James & Associates, Inc., and Raymond James Financial Services, Inc., are affiliated with Raymond James Bank, member FDIC.

![]()

INTERNATIONAL HEADQUARTERS: THE RAYMOND JAMES FINANCIAL CENTER

880 CARILLON PARKWAY // ST. PETERSBURG, FL 33716 // 800.248.8863 // RAYMONDJAMES.COM